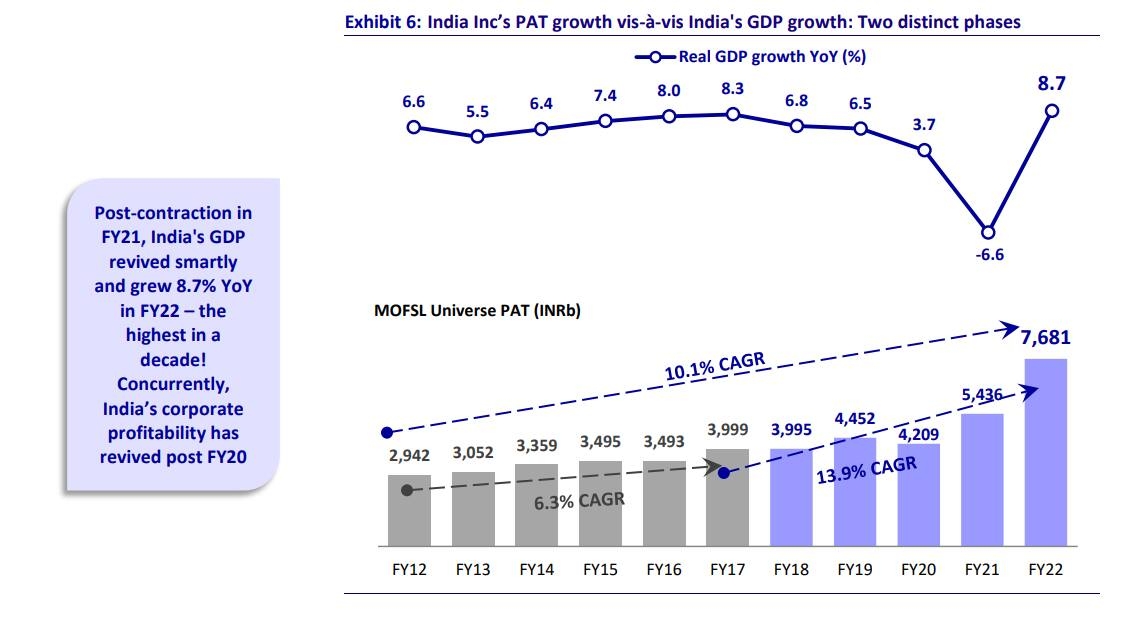

Analysing the earnings development for India Inc, home brokerage Motilal Oswal (MOSL), in a current report revealed that in FY12-22, India Inc’s earnings multiplied 2.6 occasions and reported at a compound annual progress price (CAGR) of 10 p.c.

Based on the report, India Inc’s earnings noticed two distinct progress phases:

Section 1 (FY12-17): On this interval, India Inc clocked a muted revenue after tax (PAT) CAGR of 6.3 p.c underpinned by a GDP CAGR of seven.1 p.c, knowledgeable the brokerage.

Section 2 (FY17-22): On this interval, as per MOSL, India Inc posted a better PAT CAGR of 13.9 p.c, although, GDP progress slipped to three.7 p.c.

The inventory market returns (Nifty-50) posted an 11.6 p.c CAGR underneath Section 1 and 13.7 p.c CAGR underneath Section 2, it additional identified. This translated right into a Full Cycle (FY12-22) CAGR of 12.7 p.c, broadly in keeping with the PAT CAGR of 10.1 p.c, it added.

Supply: MOSL Report

Sectoral Developments

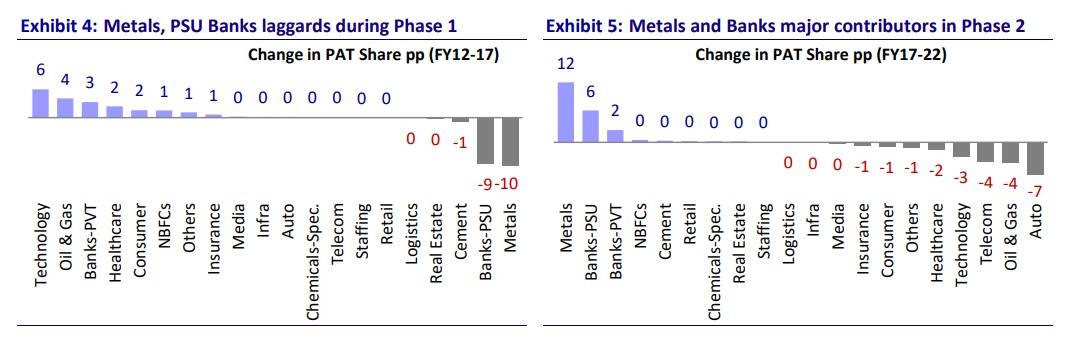

Section 1: Throughout this five-year interval, company revenue grew at a slower tempo because of a number of macroeconomic headwinds and excessive rates of interest, stated to MOSL, including that the MOFSL universe revenue registered a 6 p.c CAGR throughout Section 1 primarily led by Expertise and O&G sectors.

“Financials’ revenue recorded a 2 p.c CAGR solely because of vital decline in PSBs’ share in MOFSL Revenue pool to 1.5 p.c in FY17 from 11 p.c in FY12. Additional, Metals noticed vital weak spot because of supply-side points, weak underlying commodity costs and mining bans through the interval. Its contribution in MOFSL revenue pool dipped to eight p.c in FY17 from 18 p.c in FY12,” said the brokerage

Section 2: Throughout this era, company revenue progress recovered well fueled by tax price cuts, discount within the banking sector NPAs and post-pandemic tailwinds that drove profitability of sectors after a weak two-year base, famous the brokerage.

MOFSL universe revenue reported a quicker CAGR of 14 p.c throughout Section 2 to ₹7.7 lakh crore. Financials continued to drive revenue progress adopted by O&G, Metals, Expertise and Shoppers, it added.

“Personal Banks continued to see robust revenue progress, contributing 12 p.c to the general protection universe revenue in FY22. Metals clocked a powerful restoration in revenue share after a weak interval (FY12-17) and expanded its contribution within the revenue pool to twenty p.c in FY22 from a mere 8 p.c in FY17. Nevertheless, Cars recorded a really difficult interval with its earnings declining at a CAGR of 6.7 p.c over FY17-22 and its share in revenue pool shrinking to 2.5 p.c in FY22 from 9.2 p.c in FY17,” the information confirmed.

Supply: MOSL Report

Defensive Sector

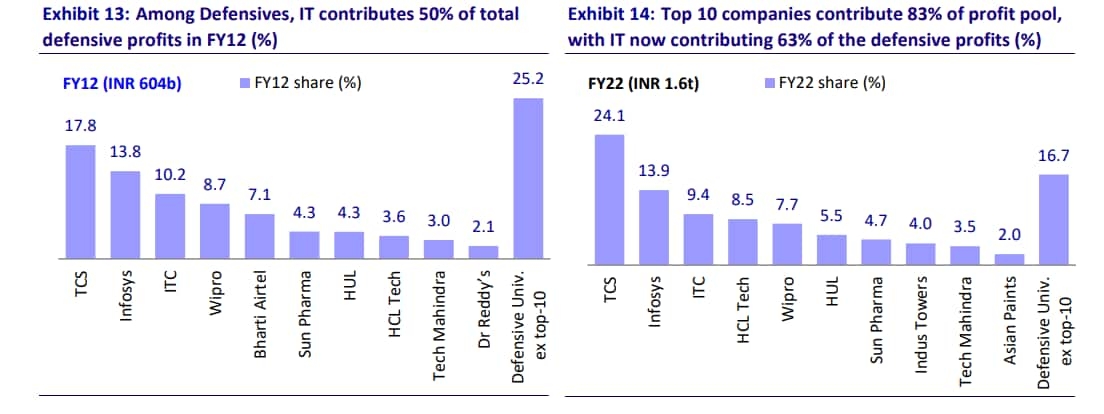

The brokerage famous that the defensive sectors reported wholesome

efficiency throughout Section 1 with 15 p.c CAGR over FY12-17 and concurrent improve in revenue pool contribution to 30 p.c in FY17 from 20 p.c in FY12.

“Regardless of a pointy moderation in progress charges in Section 2, the Full Cycle earnings progress of the defensive sector is equal to MOFSL Universe CAGR of 10 p.c over FY12-22,” added the brokerage.

Amongst shares, TCS, Infosys and ITC proceed to stay the highest 3 revenue contributors amongst defensives class, famous the brokerage. IT now contributes 63 p.c of the revenue pool of defensives, which was 50 p.c a decade again, revealed MOSL.

Bharti Airtel and Dr Reddy’s Lab, which had been throughout the high 10 checklist in FY12, had been changed by Indus Tower and Asian Paints in FY22, it said.

Telecom, which was a optimistic contributor to income in FY12 (8.2 p.c share), turned a laggard with -10.9 p.c share in FY22, it added.

Supply: MOSL

Financials

As per the brokerage, Personal Financials sector has been a star performer. The sector recorded a PAT CAGR of 14.6 p.c over Section 1 and 18.2 p.c over Section 2.

Amongst them, Personal Banks and NBFCs’ mixed PAT share climbed up 760 bps to 17.8 p.c in FY22 from 10.2 p.c in FY12 and 14.8 p.c in FY17, knowledgeable MOSL.

Auto

Whereas financials’ PAT share surged on this interval, car PAT share slid, highlighted the brokerage. The Auto sector’s revenue share moderated to 2.5 p.c in FY22; it posted an FY12-22 PAT CAGR of -3 p.c versus 10 p.c for the MOFSL universe, famous MOSL. Additional, the Section 2 PAT CAGR stood at -12 p.c versus +14 p.c for the MOFSL universe, it added.

Nevertheless, a company-level evaluation indicated that the sector’s efficiency was not as unhealthy because the aggregates steered, revealed the report. Tata Motors, which accounted for 30-45 p.c of the sector mixture sector PAT, sharply underperformed since FY17. Excluding Tata Motors, the FY12-22 sector PAT CAGR stood at 7.4 p.c, highlighted the brokerage.

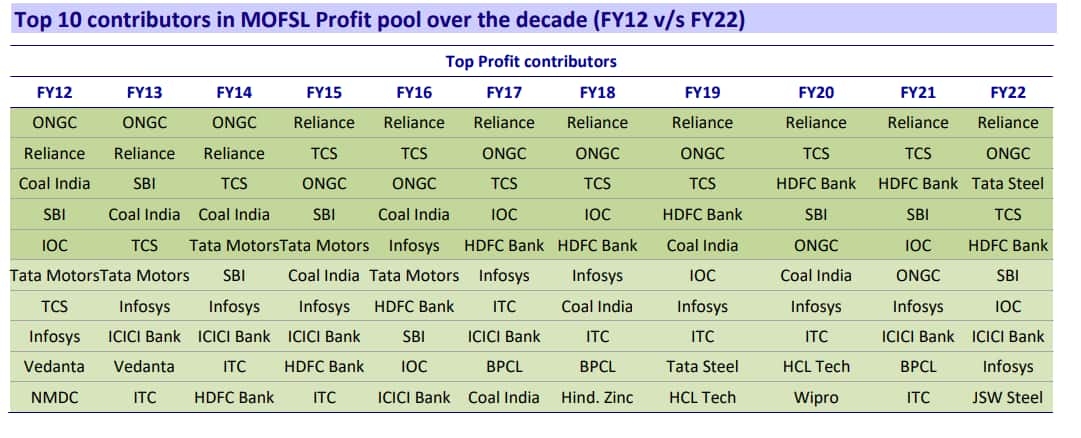

Prime 10 of the last decade

Supply: MOSL

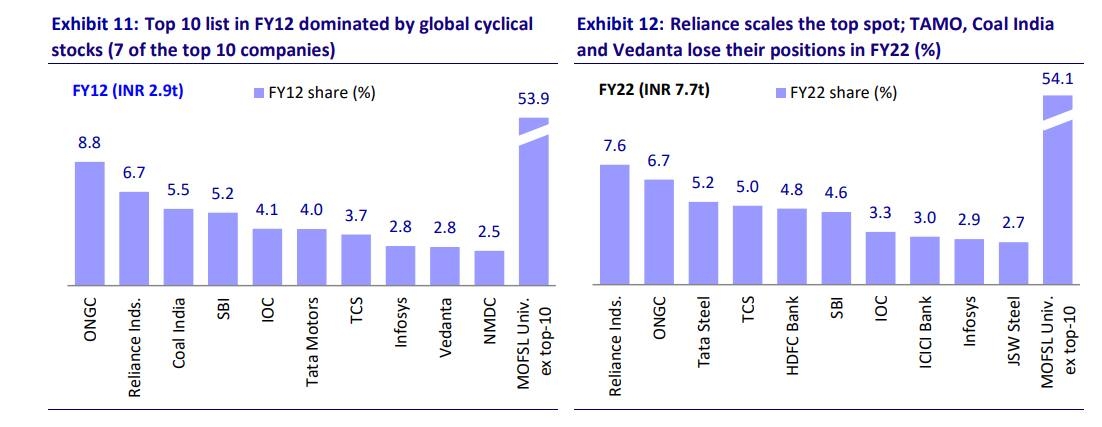

The highest-10 revenue contributors checklist in FY12 was dominated by International Cyclicals which accounted for 7 out of 10 firms. In FY22 – there are 5 international cyclical, three BFSI and two IT firms within the Prime-10 most worthwhile firms checklist, famous the brokerage.

Based on the brokerage, the highest 10 most worthwhile firms contributed 46 p.c to the MOFSL universe revenue pool.

Reliance Industries scaled the highest spot and has been occupying it for the final eight years whereas Tata Metal, HDFC Financial institution, and ICICI Financial institution which weren’t a part of the Prime-10 revenue contributors in FY12, have entered the top-10 league over time, identified MOSL.

Coal India, Tata Motors, NMDC and Vedanta had been among the many top-10 revenue contributors in FY12 however are absent within the FY22 checklist, it stated.

JSW Metal’s contribution of revenue share climbed to 2.7 p.c (from a mere 0.5 p.c a decade again), enabling it to enter the Prime-10 checklist, added the report.

In the meantime, within the BFSI area, SBI was the one inventory to be within the top-10 league in FY12 as in opposition to three shares now (HDFC Financial institution, SBI, and ICICI Financial institution), reported MOSL. It added that there’s not a single shopper firm within the top-10 revenue contributors in FY22. ITC although has been a part of the checklist for eight years throughout FY13-FY21.

“Reliance, ONGC and TCS remained among the many high 5 revenue contributors all through the last decade whereas Tata Motors dropped from among the many most worthwhile checklist (underneath Section 1), to the highest 5 loss-making firm checklist (underneath Section 2). Tata Motors now contributes greater than 22 p.c of the general reported losses in MOFSL universe. Coal India, which was within the high 10 checklist till FY20, misplaced its place within the final two years,” said MOSL in its report.

Supply: MOSL report

Loss pool rises

“Loss swimming pools have grown constantly during the last 5 years. The contribution of loss-making firms has elevated over the previous decade, which is at present at 6 p.c of the revenue pool. The Prime 5 loss-making firms contributed greater than 96 p.c of the complete losses of the MOSL protection universe,” the report knowledgeable.

Tata Motors had been the brand new addition amongst loss contributors during the last 5 years whereas Vodafone Thought was the biggest loss contributor throughout Section 2, it added.

Supply: MOSL Report

Outlook

Going forward, MOSL expects 17 p.c earnings progress over FY22-24 and the beaten-down sectors to rebound.

“India’s earnings cycle has seen a turnaround after virtually a decade and continues to stay wholesome, amid the present antagonistic macroeconomic situation with heightened worries on rising rates of interest, elevated crude oil costs and liquidity tightening that has stored the market risky and jittery,” it stated. MOSL estimates an FY22-24 PAT CAGR of 17 p.c, led by BFSI & Cars.

Supply hyperlink